Jumbo Interactive (AU:JIN)

Online lottery specialist

Robin research covers small and medium-sized companies with an attractive risk/reward profile mainly in Europe and North America.

Disclaimer: this is neither a buy and sell recommendation nor private advice. Investing in companies carries a risk of permanent loss of capital. Before investing in a company do your own research

Summary

CEO and founder owns 15% of the shares

Stable FCF generation

Turnover of $130 m and TAM of $685 b

Double digit growth

Company overview

Jumbo is a pure-play digital lottery specialist. They provide proprietary lottery software platforms and lottery management expertise to the charity and government lottery sectors in Australia, Canada and UK.

Jumbo was founded by the current CEO Mike Veverka in 1995 and listed the business on the ASX in 1999. It is headquartered in Toowong, Australia.

What it does?

Jumbo wants to be the number one company worldwide in digitising the lottery, making it easy and accessible to as many people as possible and also creating positive social value.

The company is looking for a young audience (under 50 years old) and to remove complexity in order to have a good gaming experience.

It has around 4 million active users mainly in Australia but also in the UK and Canada. In good causes it has raised $235 m in 14,000 different causes.

Although, as we can see in the graph below, most of the revenues come from the government side, Jumbo has found in the Charity side a sector that is not well covered by other competitors.

Products & services

Lottery Retailing, sale of Australian national lottery and charity lottery tickets online and on mobile devices to customers in Australia and eligible overseas jurisdictions. Address to Business-to-Consumer (B2C).

Software-as-a-Service (SaaS), development, supply and maintenance of proprietary SaaS for authorised Businesses, Charities and Governments in the lottery market in Australia and the United Kingdom. Address to Business-to-Business (B2B) and Business-to-Government (B2G)).

Managed Services, provision of lottery related services for authorised Businesses and Charities in the lottery market on a domestic and international basis. Services include technology, prize procurement, lottery game design, campaign marketing, and customer relationship and draw management. Address to B2B.

Business model

The company generates its revenue by charging a percentage of the Total Transaction Value (TTV) which is either through the lottery it directly manages or through the services it provides to third-parties.

The company has relationships with three main stakeholder groups: B2C, B2B and B2G. Let’s take a look.

Retail B2C, it operates from www.ozlotteries.com website and sells tickets in Australian national draw lottery games to customers under 10-year reseller agreements with The Lottery Corporation (TLC) which run until 26 August 2030. Also sells tickets in Australian charity lottery games under agreements with several licensed registered charities in Australia.

The Lottery Corporation (TLC) is the Australia’s exclusive operator of licensed lotteries for all Australian states except for Western Australia

One of the drivers that increases retail TTV and revenues is the number and amount of jackpots. In this segment, the company invests in marketing actions to grow and activate web and mobile transactions.

SaaS B2B B2G, this segment licenses the Jumbo lottery software platform to several customers, including to ozlotteries.com, and develops, improves, and maintains the Jumbo proprietary platform. Software licence fees range between ~3% and ~9% of ticket sales (TTV – Third-party) that are processed through the platform. This all-in-one solution is aimed at Governments and large charity lotteries.

Managed services B2B, provides lottery management services including prize procurement, lottery game design, campaign marketing, and customer relationship and draw management. These services are provided in addition to the proprietary-owned lottery software platforms to licensed charities in Australia, Canada and the UK. It is more focused on small customers.

Although historically the company has specialised in the retail sector, it is now shifting its growth strategy to a very under-served and specialised niche market, the Charity lottery. On the other hand, it has realised that managing the services and providing the customer with a platform on which to operate is very lucrative and is trying to grow there.

These two specialisations are differentiating Jumbo from its competitors to try to be a world leader here and become the platform of reference.

What makes the Jumbo model interesting? The magic of this business is that both parties are perfectly aligned.

In some countries the practice of selling lotteries for a good purpose is widespread and well accepted by the population such as US, UK, Canada or Australia. Charity seek to finance themselves with as much stability as possible and see the lottery as a plausible way, as donations do not always come in.

The difficulty is to create and manage a lottery system without knowledge and without funding. That is why Jumbo's solution works so well as the company helps these non-profit organisations to manage the whole process end to end. The Charity gets stable funding without putting any money in and Jumbo earns a percentage of each transaction.

The more effort both the Charity and Jumbo put into in promoting and developing the lottery, the more money both parties make.

Market trend

As you can imagine, this is a market regulated by the local governments of each region and/or country. Furthermore, we are talking about a digital lottery market, something that is not highly developed in most countries and that is gradually increasing its penetration due to the changes in trends.

Australia currently sits at 38.4% digital penetration for lotteries. This compares to 45% in the UK and well over 50% in some European countries. This trend towards purchasing lottery tickets online will continue, bringing digital lotteries to a broader and younger audience. Some studies indicate that the growth of online lottery over the next few years is 5% CAGR.

What is more the TAM in the US, Australia, Canada and the UK alone is $685 bn.

Jumbo has estimated that with current products and services it could reach a maximum market volume of $10 bn. Imagine the number of new products and services that could be launched... it would be practically decades of growth!

It is interesting to note that one of the great opportunities is completely untapped. I am referring to the Charity sector in the United States. At the moment this market is not possible to enter due to lack of regulations and the company has been preparing for years when the opportunity might open up. The graph above shows the potential size of the US market. Impressive.

Another aspect I would like to point out is how the online channel is gradually gaining ground over the traditional channel. At the end of the day, everything we know is going digital and customers are going to need these developments as everything is moving in the same direction.

It is an unstoppable movement, in countries like Poland 70% of the lottery is already online. In contrast, other countries are still at 5-10% of online sales... if we think about it, there is still a lot of ground to cover. Good news for Jumbo.

Finally, it should be noted how resilient this market is, even in the worst crises of all kinds such as 2008 or Covid, sales continued to grow. At the end of the day, it is a minor expense and represents a ‘hope’ that society as a whole sees as acceptable.

Growth strategy

The company combines organic and inorganic growth. Over the last 5 years the company has grown by around 25% YoY by doing this combination. Even without M&A it is able to grow organically at double digits.

To grow organically Jumbo uses three strategies:

Maximising the potential of our existing business and product portfolio

Replicating best-practice operations and build for global scale

Diversifying its portfolio to unlock incremental TAM opportunities for example in other industries such as banking, music, accommodation, housing and car sales.

The company believes it can grow strongly in the markets where it is already present: Australia, UK and Canada as there is still plenty of room for penetration. These territories are their priority.

The company is also monitoring the US market where the digital lottery is completely undeveloped. Being the first to land there would be a great success for future growth. For the time being, however, we must continue to wait without a clear time frame as to when it will be possible to operate. However, the company's growth plans include the US market as a secondary priority.

One of the keys to growth is to progressively increase the number of players accessing and purchasing lotteries through the digital platform. The company note that with the increase in SaaS and Managed services since 2020 there has been a strong increase in users from countries other than Australia.

M&A

Since 2019 the company has made three acquisitions; Gatherwell and StarVale in UK and Stride in Canada. The aim was to grow internationally in these territories.

The three acquisitions have characteristics in common, suggesting that Jumbo is consistent with its M&A strategy of recent years:

In all cases it maintains the original company's key Management. Even the founder when possible

They are SaaS or Managed services companies oriented to Charity

It allows access to a new market

Bought between 5-7x Net Profit After Tax (NPAT) in cash or debt

Acquisitions of small/medium sized companies

Jumbo sees these acquisitions as a way to make itself known quickly and reach new customers outside Australia. A strategy that, if well executed, can accelerate its growth.

Management

One of my favourite layers of security is to look at whether a company is led by its founder and whether he holds an interesting percentage of shares in the company.

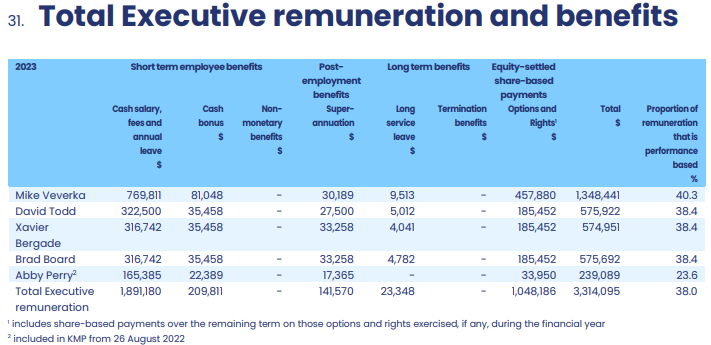

CEO and founder Mike Veverka owns 8.9 million shares (15% of the company's total) which translated at the current market price would be close to a value of almost $100 M.

On the other hand, an important part of the board's salary is in stock-based compensation according to the company's performance. This is positive because it aligns the management team with the shareholders and has one point that I like less and that is that a small percentage of the shares is diluted.

However, I believe that the board is effectively aligned with shareholder interests. Also, the management that is key to the success of the company has been in place for > 20 years.

What can go wrong?

Here I see two relevant risks, the first being the regulatory framework and the second the credibility and image of the company.

From a regulatory point of view, on the one hand, it can prevent the entry of new competition, as governments are responsible for managing licences or authorising company purchases. On the other hand, there would be a risk that governments would start regulating online lotteries in order to avoid major evils in society, such as gambling addiction.

Fortunately for Jumbo, however, the lottery has a friendlier image than an online casino, for example. It also affects a large majority of the population who are looking forward to spending a little bit of their money every week on a recurring basis. I don't think governments would want to introduce unpopular measures here as there would be other priority issues.

Regarding the loss of credibility and image, a failure in Jumbo's system could have serious consequences since, as mentioned above, a large majority of the population regularly plays the lottery. For example, 70% over 18s play lottery regularly in UK.

If it turns out that Jumbo's platform is seriously flawed or unable to provide a good service with jackpots, it could generate discontent among a wide population that would reach the government, and the government could take action against Jumbo.

Final takeaways

Jumbo is a company with impressive metrics.

Growth of 25% on average over the last 7 years combining organic and inorganic growth.

Operating margins of 40%, ROE >30% and ROIC >40%.

Dividend payout progressively increasing over the years

It is an asset light business, its Capex is practically zero

Negative debt and generation of very solid FCF and growing margins

It also has a good management team loyal to its founder and, as we have seen before, aligned with shareholders

Huge TAM to conquer and tailwinds from the era of digitalisation and AI

It is true that the numbers reflect the business we have in hand. Of course the market is not going to put this company at a knockdown price.

I have researched companies similar to this one but have not been able to find any that are listed on the stock exchange. There are some lottery companies but they are classic mode and it is not possible to compare them with Jumbo.

In my opinion Jumbo is building its MOAT right now by seeking to be a reference in the Charity niche market in Anglo-Saxon countries. What will make it stand out from the rest is the quality of its platform and above all its brand as a reliable company and market reference. If Jumbo manages to maintain this credibility, it could become the “Evolution” of the lottery segment.

I hope you liked it and see you next time! Please comment and I will try to answer any questions you may have.

Thank you!

could you please provide names/tickers of the listed lotteries, that you found?

"

I have researched companies similar to this one but have not been able to find any that are listed on the stock exchange. There are some lottery companies but they are classic mode and it is not possible to compare them with Jumbo."

What is the competitive advantage comparing to The Lott app from TLC? Jumbo is selling their tickets with higher price. Why should I buy tickets with them?