Robin research covers small and medium-sized companies with an attractive risk/reward profile mainly in Europe and North America.

Disclaimer: this is neither a buy and sell recommendation nor private advice. Investing in companies carries a risk of permanent loss of capital. Before investing in a company do your own research.

Key data

Family-owned and operated for more than 40 years.

European market leader.

Sustained growth even in times of crisis.

Margin widening as it gains scale.

Company overview

Trigano is an European company specialising in the design, manufacture and distribution of recreational vehicles (RV), trailers, mobile home and accessories.

The company was founded in 1935 and is based in Paris, France.

A long history

It is worth mentioning the long history of this company, which was founded by the Trigano family, who began their activity in France by selling canvas for tents, focusing on something that did not exist at the time: paid holidays.

Later, the Trigano family expanded the business to include the distribution of camping and sports equipment, and in 1971 the caravan business was born.

Since then, the company has continued to develop in this sector.

Products and services

Trigano has a portfolio of 27 brands which can be divided into products, services and accessories.

Products

Motor homes

Compact Vans: this is the most compact vehicle, often fitted with a pop-up roof. Seen by many as a large family car, it is discreet, handles well and is popular with families, often younger than those who buy other motorhomes.

Vans: longer than a compact van but shorter than a low-profile vehicle, this offers the same as a low-profile vehicle with a more compact size. It also has the metal coating of a compact van. Customers tend to be families and lifestyle and sports.

Low profile: it has a fitted cabin chassis with a unit made from composite materials. It offers even better habitability capacities than vans and tends to be used by newly retired people.

Capucine: this is a low profile vehicle which has the peculiarity of having a double bed positioned directly above the driver. It is a very popular product with car renters and families of 4 or 5.

A-class: the best habitable vehicle made up of composite materials and polyester. This is the luxury motorhome aimed at repeat travellers with a passion for motorhomes.

Motor homes. Source: Trigano

Caravans: rigid touring, living caravans and folding caravans.

Mobile homes: from canvas structures to mobile homes, a wide range of outdoor accommodation for professionals (campsites, tour operators) and private individuals alike, combining design, comfort and reliability.

Trailers: the company manufactures and markets luggage and utility trailers for private and commercial customers.

Trailer. Source: Trigano 5. Garden and Camping equipment: outdoor games (porticoes, swings, slides), open-air pools, carports; tents and camping furniture for individuals, as well as for communities and outdoor hotels.

Services and accessories

6. Services: rental of motor homes, the financing of all leisure vehicles and a range of rental stays in mobile homes. Finally, after-sales support.

7. Accessories for leisure vehicles: accessories and spare parts to complete the equipment of recreational and daily maintenance of recreational vehicles.

Sales are mainly concentrated on motor homes and caravans, and the company is now looking to grow in mobile homes. The majority of sales are made in Europe.

During 2023 Trigano was able to sell a total of 67,200 leisure vehicles and more than 110.000 trailers.

Business model

The business model is simple to understand: products are produced in the factories (with the help of suppliers and OEM), then they are distributed and stored, and finally the customer accesses the product through an own or independent commercial network.

These products and services are aimed at providing the customer with an experience of freedom, simplicity and good times with family and friends.

To achieve this, Trigano has created a parent company that facilitates the day-to-day running of the operating companies. This frees the operating divisions from the need to maintain technology systems, manage insurance, share best practice, define strategy and objectives, and manage new acquisitions, and allows them to focus on running the local business effectively.

Market trend

The global camping and caravanning market size was estimated at $53.1 billion in 2022 and is expected to grow a CAGR of 10.4% from 2023 to 2030.

In Europe camping and caravanning market size is estimated at $16 billion in 2024, and is expected to reach $29 billion by 2029, growing at a CAGR of 11% during the forecast period 2024-2029.

New lifestyles, in particular spending time in outdoor activities that are more environmentally friendly and relatively affordable for the customer, are making the market grow rapidly. During Covid, sales declined, but recovered strongly because you may be more isolated from other people than if you were staying in a hotel or an apartment, for example.

We could even think that people who had not tried it before thanks to Covid started their first experiences and liked feeling more connected to nature and living healthy experiences with their families and friends.

According to Trigano, its Europe customer base is young seniors between 55-65 years old who are more likely to escape in the low season and off the beaten tourist track. In North America, 12% of camping enthusiasts own an RV nearly half are between 45-54 years old with a median household income of $76,000 or higher. However, the younger consumer base under 39 years of age is increasingly gaining ground.

The age of the average consumer is an important point, as the trend in both Europe and North America is towards an increasing proportion of people in the older age bracket.

This will be a key driver for Trigano's future business.

Globally, the camping business is concentrated in Europe and North America, the first being the largest market in terms of sales and the latter the fastest growing market. Regions such as Asia are also experiencing an increase in demand from their populations, driven by a growing middle class. Growth in the region is estimated to exceed 10% CAGR over the next few years.

With regard to the registration for motor homes and caravans in 2023, it is noted that has been reduced by -7.6% and -13.8% respectively, mainly due to difficulties in the supply of chassis by car manufacturers.

I checked the registrations for the 2018/2019 season and they were 132,000 motor home units and 78,500 caravans. The latest data for the season 2022/2023 are 160,000 motor home units and 61,000 caravans registered so we could argue that there is a process of stabilisation. The data from 2024 until march confirms that there is stability in the number of registered vehicles; 2,800 more units than the previous year.

Does RV manufacturers have pricing power?

We can confirm that yes. I have selected the sales data and units sold by Trigano in 2019 and 2023. In 2019, the average sales price of an RV was €40,000, while in 2023 it is €53,000; +32%.

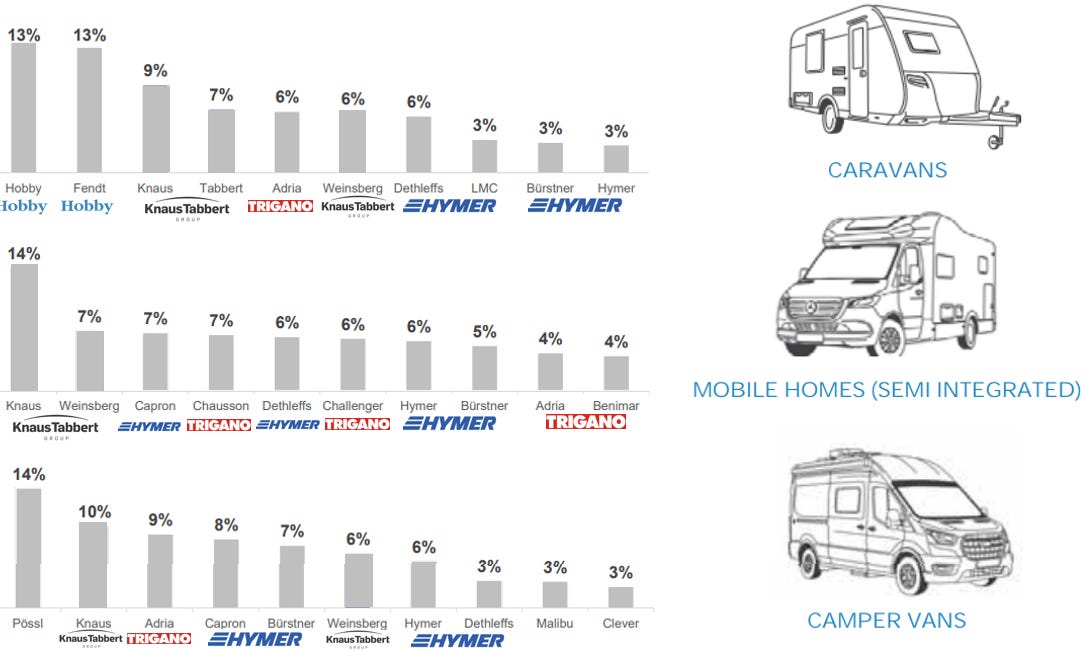

European competition

In the chart above we can see some segments and their strongest competitors.

We can see that almost all the players with the largest market share belong to one group: Erwin Hymer (Thor), Knaus Tabbert and Trigano. There are very few independent companies at the top.

Now let's aggregate all market segments and then we will get a different ranking. A new player is now also added; Rapido Group.

In 2023, around 200,000 motorhomes and caravans will be sold; in this chart above, these five companies will sell around 177,000 units. This represents 88% of the specific RV market; a concentrated market, an oligopoly.

The two dominant companies are Trigano and Erwin Hymer (Thor) with more than 50% of the market. The difference between the two is that Trigano has opted for an entry-level product for caravanning starters at a lower price and it dominates southern Europe in particular. Meanwhile Erwin Hymer (Thor) dominates northern Europe with more traditional brands, where customers value quality over price.

Fortunately for us, three of the four companies are listed on the stock exchange so we can study their indicators to understand the quality of these businesses.

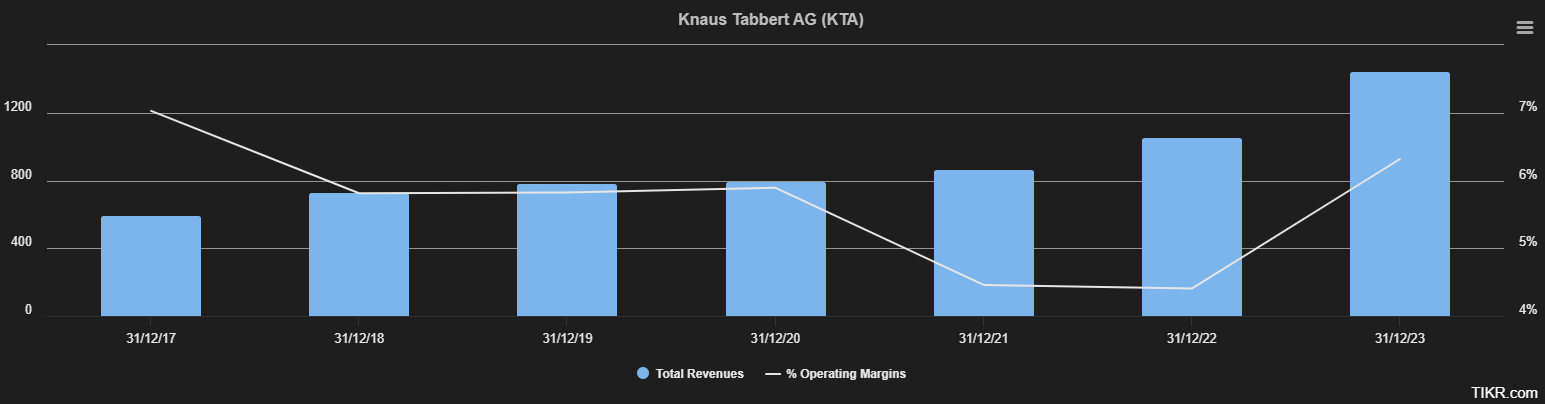

Knaus Tabbert and Trigano have better growth as they are smaller companies.

In terms of return on equity there is not one company clearly of higher quality than the other as it is a bit spread out. At least each of them enjoy more than acceptable returns; ROE of > 15% and ROCE of > 19%.

One qualitative difference between Trigano and Thor is its sensitivity to the cycle.

The graphs below show how Trigano maintained its sales level and margin very well during Covid, while Thor's operating margin collapsed. In fact, Trigano's operating margin continues to evolve year on year. It is important to look at margins, but more importantly to look at how they are evolving over time. This gives us an indication that the company has a competitive advantage over its competitors.

On the other hand, we have Knauss Tabbert, which has less of a track record on the stock market but has a different business model in that it makes virtually no acquisitions and all its growth is organic; the opposite model to its competitors. It is interesting to see how it has stable and even growing sales.

Trigano and Thor the serial acquirers

Both companies are "beasts" when it comes to acquisitions. In Trigano's case, they sometimes say that they buy companies or assets that are in financial difficulty.

Looking at the lists below, it is striking how they have continued to do M&A year after year in a really difficult environment, when other sectors simply stopped because of high interest rates.

Are we facing a declining business in which only a few companies can survive? At the moment, the data tell us yes. Trigano ensures the survival of those companies that would have disappeared on their own, hence the super M&A activity in the difficult years.

Finally, Trigano and Thor have pursued different strategies in recent years with regard to M&A and partnerships. While Trigano has recently focused on investing in expanding its distribution network, Thor is concentrating on developing electric RV.

Historically, both companies have a strategy in common of vertical integration of the industry, from distributors, manufacturers, components, accessories and spare parts.

Growth strategy

Trigano says it clearly: gain market share.

As we saw in the previous point, this is done through strategic acquisitions across the supply chain and in complementary and/or adjacent product categories.

Products affordable, the company is positioned in the segment of vehicles for beginners rather than experts. It is therefore essential for Trigano to offer a good price without undermining margins. This is achieved through cost control, economies of scale and further integration of the value chain from production to sales and after-sales.

New products, usually by buying other companies to offer their customers new products, such as the recent BIO Habitat deal; as a growth strategy in the mobile home business.

Electrification of leisure vehicles, this is vital to develop these products in order to be aligned with the thinking of its own customers, to have a healthy and sustainable out-of-home experience. Regulation in Europe may also be getting tougher in this respect.

Competitive advantage

Power pricing, it is able to pass on cost increases to the final consumer. However, this is limited by the price elasticity of demand.

Industrial organisation, can achieve economies of scale during manufacturing and improve its response to raw material inflation due to its size. As a curiosity, the effect of rising energy prices does not affect it as it is an industry that needs little energy to produce. The management of external manufacturers of some components is key to ensuring that production does not stop. The larger the scale, the greater the bargaining power.

Distribution network, especially in southern Europe, is dominant in this area. It works with more than 1,200 sales outlets.

Cross-selling, is able to sell to the same customer, the product, complements, accessories, repairs, spare parts, financing, etc. This is very powerful as you can extract more value per customer than if you were to focus on just one category. It also allows risk to be spread across more categories and even improve the seasonality of the business.

Culture, the great forgotten but I could not imagine a company of such quality if this was not being taken care of by the management. It is not possible to integrate 38 external companies into your organisation without this important gear.

Serial acquirer profile, along with Thor, the most experienced company in the sector in acquiring businesses, even in bankruptcy. This gives credibility in the market when Trigano wants to buy a company. He has done it so many times that it is an essential process in his DNA.

Management

The Feuillet family has been in control of the company since 1981 and has developed and managed the business model over the years. They also made their fortune by being majority shareholders for 40 years.

Mr. Francois Feuillet was at the helm until 2020; today is member of the Management Board. In 2021, Stéphane Gigou, former head of Fiat, was chosen to succeed him.

In total the Feuillet family own more than 57% of the shares which at the current share price would be close to €1.2 billion in value. Now that's skin in the game!

What can go wrong?

Supply chain disruptions can lead to price increases for products that consumers do not want to pay. This recently happened in the trailer segment:

“After several years of growth in the post-Covid period, the segment was heavily impacted by the rise in steel prices, which pushed selling prices upwards”

Although the company has pricing power, there is a limit as it is a discretionary product.

On the other hand, we have regulatory issues in the sense that the French regulator has on some occasions forced Trigano to divest from certain areas because it considered it to be in a monopolistic position. I don't see this as a major problem given the history of the company, but it's something to keep an eye on and monitor.

Now, for example, we have the case of BIO Habitat (strategic acquisition), which is awaiting approval from the French authorities. In fact, this approval is long overdue and should have been granted by now. This is slowing down Trigano's ability to implement its strategy.

As far as the electrification of products is concerned, I don't see much progress at Trigano. However, its big competitor Thor is making efforts and this could be the key to sales in the long term. I don't see it as a threat at the moment, but it's something to consider as a long-term trend.

Final takeaways

I enjoyed writing about this case because it is a surprisingly resilient sector even in an environment of inflation, high exchange rates and supply problems, the company and the sector in general are doing well.

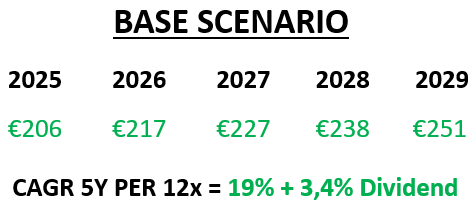

It is currently trading at 6x forward PE. I think the company is worth at least 10-12 times earnings, and if it can maintain high single-digit growth and expanding margins, I think the multiple should widen.

Light capital business, no debt with cash, FCF generation to continue making acquisitions, sales growing mid-high single digit, margins expanding, founding family at the helm… What more could we ask for?

To calculate the returns, I have used sales growth of just 5% (I think it could be 8% in the next few years) and an EBIT margin of 12% (although I think it could be 13-14%).

The company has a dividend policy of increasing over time.

Another story would be if the company surprised us with a major acquisition in North America or even expanded into Asia; is a possibility although I have not read it from Trigano.

I hope you have enjoyed this interesting section! As always, I invite you to participate in the comments section or by writing to me directly. See you soon!

The problem with Trigano relatively to Thor is that it requires much more working capital and has more difficulty as a result in generating the same FCF generation. What is your view on Trigano's working capital needs? They seem really high

You should take a look at Lazydays (GORV)