Valtecne SpA (IT:VLT)

Small gem in high precision mechanical market

Robin research covers small and medium-sized companies with an attractive risk/reward profile mainly in Europe and North America.

Disclaimer: this is neither a buy and sell recommendation nor private advice. Investing in companies carries a risk of permanent loss of capital. Before investing in a company do your own research.

Company overview

Valtecne is a contract manufacturer of high precision mechanical components as a first, second or third level supplier of Original Equipment Manufacturer (OEM).

Founded in 1983 by Mr. Paolo Mainetti, today it is his son -Vittorio Mainetti- who heads the company. The company's headquarters are located in Province of Sondrio, Italy.

Products and services

The company operates in two lines of business: Medical and Industrial.

Medical line, focused on the manufacturing of complex surgical instruments for joint reconstruction (hip, knee and shoulder), spine surgery and trauma. Some of the products, due to their small size and the materials used (stainless steel, titanium, etc.) require the use of sophisticated technologies.

Industrial line, dedicated to the production of high precision mechanical components for power transmission, automotive and energy segments.

Finally, the company offers its customers its technical department and engineering that supports the design process for its customers.

Business model

Valtecne carries out the entire end-to-end production process (turnkey), purchasing the raw materials, carrying out the industrial manufacturing process (assembly, quality check, etc.) and logistics. However, the company's business model is flexible and it can adapt processes to the individual needs of its customers in the form of co-design.

Valtecne's customers are medium and large companies leaders in their respective markets. For the Medical line the company deals with manufacturers of orthopaedic prostheses operating both locally and globally. On the Industrial side the company operates as tier 2 or tier 3 in different supply chains for industrial groups such as Caterpillar, CNH or Toyota to mention just a few.

The business line with the highest turnover is Medical (60%) as the company is putting its efforts to grow here in recent years. Why? This segment has a shorter supply chain and better margins than the Industrial line.

A distinguishing feature of this market is to win a new customer, high precision mechanical companies need to go through a qualification process proposed by the potential customer. These qualification processes could take a year to complete and involves multiple steps and efforts between customer and supplier. This is not surprising as the product is so peculiar, complex to produce, with very exact specifications that cannot fail and sometimes regulated by law (especially Medical line). This creates a barrier to entry for competition and keeps the client captive, as the client does not want to go through the qualification process again and change supplier because of the risk and work involved.

Market trend

The company's main markets are orthopaedics and power reducers (or gearboxes) for industrial machinery.

Orthopaedics market

Focused on the creation of the surgical instruments essential for implanting prostheses during orthopedic surgery.

It is a market characterised by high resilience and low volatility. It makes sense, although an orthopaedic operation is not life-threatening and could be postponed; the patient's quality of life is poor because he or she will be in pain and his or her freedom of movement will be limited. An emergency operation cannot be postponed.

The orthopaedic market currently has a volume of around $60 bn and is expected to grow at 2-4% CAGR until 2026. Valtecne covers 82% of the total market segments with its product portfolio.

By region, the leading market is the USA with 66% market share, followed by EMEA with 18%. Finally we have APAC countries with 13%.

The main drivers of growth are related to the ageing population, increasing global wealth and the increasing effectiveness of surgeries due to technological advances.

Gearbox and hydrogen vehicles market

The size of the gearbox market is approximately $32 bn and is expected to grow at 4.5% CAGR until 2028. This market has interesting tailwinds from the global adoption of industrial automation and, on the other hand, from increased industrialisation in emerging economies.

In addition to this market, the company is active in solutions for hydrogen-powered vehicles. The company produces high-precision components for fuel cell valves for tier 1 suppliers of automotive OEMs - such as Bosch, Honda, Toyota and others - involved in the hydrogen supply chain.

This market has a bright and strong future ahead of it; the market is expected to grow at a 2021-2028 CAGR of 53.5% reaching the amount of $34 bn by 2028.

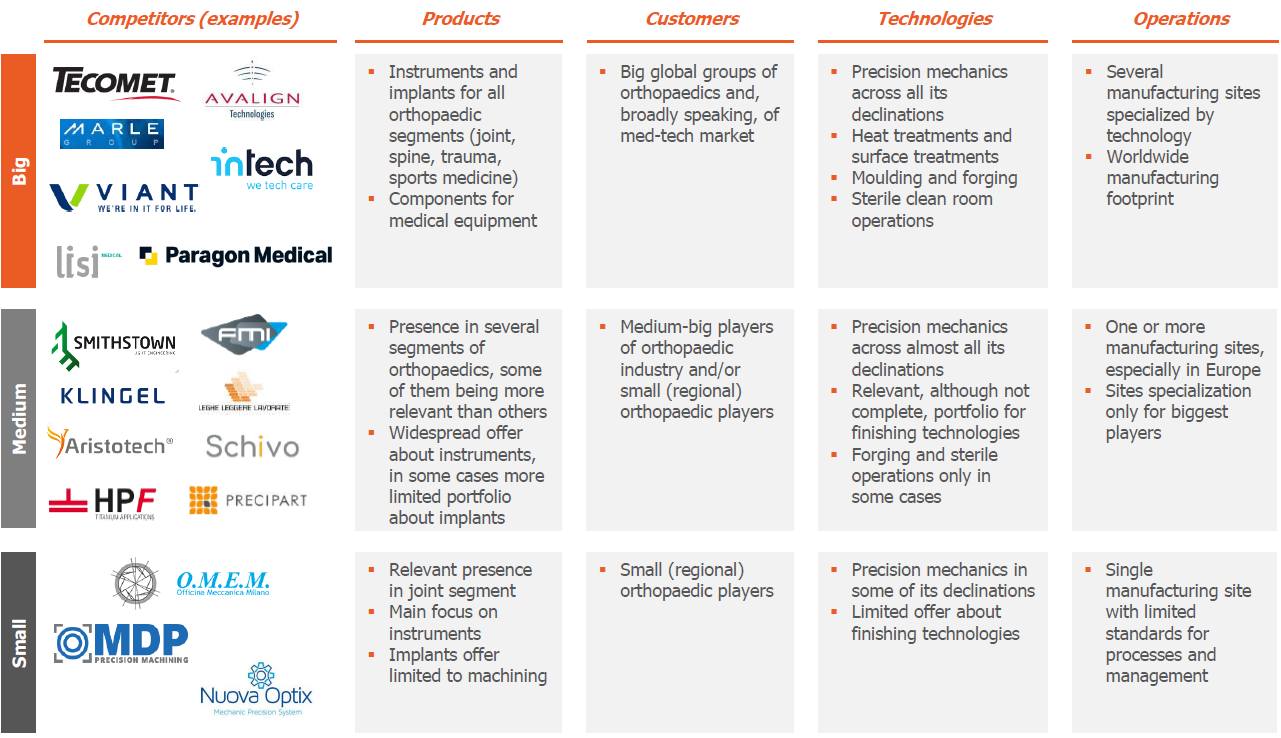

Competition

Above is an interesting analysis of Valtecne's competition. Companies comparable to Valtecne would be those located in Medium size (revenue between €10 to 100 m).

Unfortunately, none of these companies are listed on the stock exchange, so it is difficult to extract a benchmark as they are private equity companies.

As an exercise we could compare with the Lisi company which has a Medical division. In addition to instruments, they manufacture implants and are also specialised in the robotic mini-invasive surgery segment. Lisi Medical achieved year-on-year growth in 2023 of 20.8% in sales and EBITDA of 17%. Valtecne would have a similar growth and EBITDA margin to Lisi Medical.

Growth strategy

The company has defined a plan for growth based on the following axes:

Reaching more customers, there is an opportunity to improve the sales force department and win new customers. The company's marketing and sales strategy also needs to be reviewed.

Expanding product offerings, increase production capacity and internalise some outsourced key processes. Also on the industrial side, reaching new market niches such as luxury cars or energy transition.

M&A, small acquisitions of companies would complement the current portfolio of product and make it easier to reach new customers. It also reviews the possibility of entering new adjacent markets where the company does not yet have access.

Operating performance, through the revision of production processes and new machinery.

It is an interesting case because we are at what could be a great beginning. In addition to improving the product mix, entering new markets and buying up smaller competitors, the company is thinking about manufacturing its own medical devices. It would therefore no longer be a supplier but a manufacturer.

Management

The company is founded and governed by the Mainetti family for 40 years. Approximately the 82% of the shares are in the hands of the family and the rest is free float.

The value of these shares at the current share price would be around €30 m whereas the total annual salary received by the entire board of directors is €800 k.

This is relevant because we can deduce that whoever is in charge of the future of the company has a lot to gain or lose depending on the future performance of the stock market.

Risks

Low stock market track record, this is certainly the main problem for me as we only have a track record of 1 year at the moment. I usually like to see at least 5 to 10 years of track record to get an idea of how the business model behaves in different economic cycles. Moreover, we do not have a clear picture of how management thinks and what its policy towards shareholders will be.

M&A, I really like companies that are able to consolidate the market by buying other competitors. The company has said that one of its growth axes will be small acquisitions to reach new customers and market niches. In this case we do not know any previous track record of whether the company has successfully executed these integrations or whether it has been able to buy at the right price these new acquisitions.

Final takeaways

Last year I kept an eye on all the IPOs coming out of Italy.

Italy is a country I pay attention to because it has good companies, the market is one of the cheapest in my investment world (Europe, North America and Australia) and sometimes they come to the market extremely cheap.

Valtecne seemed to me about 1 year ago the most interesting company of the Italian IPOs in 2023 and I kept following it until today when I decided to talk about it.

What I appreciate most about this company is its history, management and plans for the future in a very special market segment. The Medtech segment - where the company wants to grow more strongly - is lucrative, has high barriers to entry and, in some ways, the relationship with customers is rather long-term because of the high switching costs to other suppliers. Moreover, the company plans to market its own products in the future (it will probably need some acquisitions to do so).

It is clearly a riskier idea than usual on the blog due to the lack of track record on the stock market, but at the same time it is very interesting to follow as it is the only company that currently offers the opportunity to invest in this very special sector.

Let's look at the data we have available to try to find out if the company has a competitive advantage.

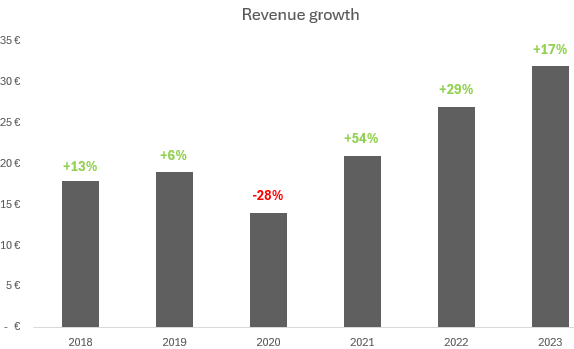

The first thing that is striking is that the company has been growing at double-digit rates in recent years. Moreover, this growth is of the highest quality - organic - and far exceeds the market growth of recent years.

We can also see how it performed in the 2020 crisis with a reduction in sales of -28%. EBITDA halved that year and had a FCF of €-0.5 m. Normally I like to see a company that does not suffer so much in crises, although I recognise that the Covid crisis was very peculiar. To the company's credit, it grew strongly the following year (it seems that customers can't wait too long to delay a purchase) and the subsequent years have seen growth slowing to a more logical pace. In my projection calculations for the future I have assumed that the company grows organically at 12% + 3% inorganically.

On the other hand, the EBITDA margin has increased from 15 to 18% today in only 5 years. It makes sense as the company is betting on the Medical sector which has a wider profit margin than the Industrial sector. For our projection we can assume that Valtecne will continue to improve this margin by positioning itself more in the Medtech sector and even selling its own products as a manufacturer.

Valtecne has net debt and it is foreseeable that in the coming years they will invest in more Capex as it is part of their growth plans to invest in machinery. ROE and ROCE 2023 would be 16% and 26% consecutively (without goodwill - no acquisitions right now).

To conclude we can say that the company steals market share from its competitors (it is growing faster than the market), has a good management of its accounts, is not leveraged and is preparing a plan to start acquisitions. It is also capable of further improving its margins, especially if it manages to sell directly to the end user and become a manufacturer.

I hope you enjoyed the reading, this case is a bit different than previous and interesting. See you next time!

Thank you for your analysis . For a small company it is always easy to gain market share. It is a nice business, but not an interesting one to invest in. Too slow market growth over all. Too concentric on two niche segments, while only one is leading to a solid EBIT Margin. Concentrating on only the surgical segment, however, holds many risks. Dont know if their would be other segments where they could entry and also win share.